Crédito: fuente

The already sputtering economic rebound went into reverse in December, as employers laid off workers amid rising coronavirus cases and waning government aid.

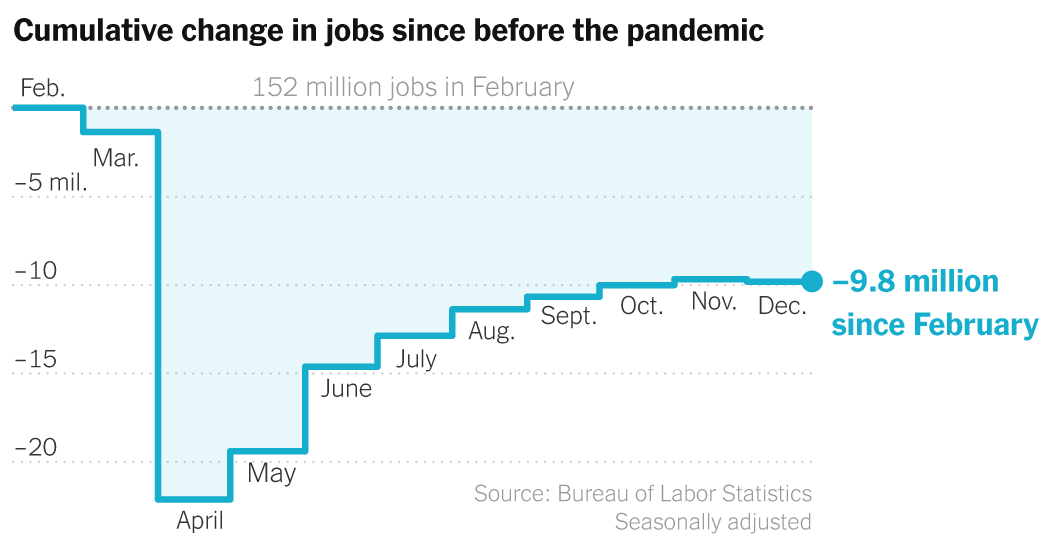

U.S. employers cut 140,000 jobs in December, the Labor Department said Friday. It was the first net decline in payrolls since last spring’s mass layoffs, and though the December loss was nowhere near that scale, it represented a discouraging reversal for the once-promising recovery. The U.S. economy still has about 10 million fewer jobs than before the pandemic began.

The December losses were heavily concentrated in leisure and hospitality businesses, which have been hit especially hard by the pandemic. The industry cut nearly half a million jobs in December, while sectors less exposed to the pandemic continued to add workers.

The unemployment rate was unchanged at 6.7 percent, down sharply from its high of nearly 15 percent in April but still close to double the 3.5 percent rate in the same month a year earlier.

Unemployment rate

By Ella Koeze·Seasonally adjusted·Source: Bureau of Labor Statistics

The new year won’t bring much relief, at least right away. The virus is still raging out of control, leading cities and states to reimpose restrictions on businesses and leading consumers to pull back on activities that could put them at risk. Many forecasters expect more weak economic data for January and February.

“I can’t see that the labor market is going to get a whole lot better until we get the pandemic under control,” said Erica Groshen, a Cornell University economist and a former commissioner of the Bureau of Labor Statistics.

The December data, the last of President Trump’s time in office, marks the end of a year of violent swings in the labor market. Employers cut 22 million jobs in March and April, then began rehiring furloughed workers en masse in May and June. By August, the economy had regained close to half of the lost jobs.

But momentum soon faded. Hiring has slowed every month since June, and the economy lost about nine million jobs in 2020 as a whole, the first calendar-year decline since 2010 and the worst on a percentage basis since the aftermath of World War II.

Congress last month passed a $900 billion relief package that will provide temporary support to households and businesses and could give a boost to the broader economy. And in the longer run, the arrival of coronavirus vaccines should allow the return of activity that has been suppressed by the pandemic.

But the vaccine and the aid came too late to prevent a sharp slowdown in growth.

“We did have a pullback in the economy,” said Michelle Meyer, head of U.S. economics at Bank of America. “If stimulus was passed earlier, maybe that could have been avoided.”

The lost winter could have lasting implications. Temporary furloughs have increasingly turned into permanent layoffs as the pandemic has dragged on, and tens of thousands of small businesses have closed for good. Millions have joined the ranks of the long-term unemployed, and in recent months many have been leaving the labor force.

When the economy shut down last spring, many workers thought they would be out of a job for a few weeks, maybe a couple of months.

Nine months later, many still aren’t back on the job.

The Labor Department’s monthly jobs report on Friday showed that nearly four million Americans had been out of work for more than six months, economists’ standard threshold for long-term unemployment. That was up by 27,000 from November, and roughly quadruple the number before the pandemic began.

Those figures almost certainly understate the scope of the problem. People who aren’t looking for work, whether because they don’t believe jobs are available or because they are caring for children or other family members, aren’t counted as unemployed.

The number of people who have been unemployed long-term is still rising

Share of unemployed who have been out of work 27 weeks or longer

By Ella Koeze·Seasonally adjusted·Source: Bureau of Labor Statistics

When the data was collected in mid-December, many of the long-term jobless faced a frightening deadline: Federal programs that extended unemployment benefits beyond their standard six-month limit were set to expire at the end of the year. The aid package later passed by Congress and signed by President Trump extended the programs, but by less than three months.

Long-term joblessness was a defining feature of the last recession a decade ago, when millions eventually gave up looking for work, in some cases permanently. If that pattern repeats, it could have long-term consequences, particularly for people with disabilities, criminal records or other characteristics that make it hard to find jobs even in the best of times.

“These are the kinds of workers who are really only recruited and called upon in a very tight labor market, and it may take us a long time to get back there,” said Julia Pollak, a labor economist with the hiring site ZipRecruiter. “That is the worry, that there are these groups of people who will drop out now and who will only really find good opportunities again after a sustained and lengthy expansion.”

-

Wall Street was poised for another gain on Friday, as investors continued to bet on robust fiscal stimulus coming from a Democratic-led government in Washington, shaking off a grim employment report for December.

-

The S&P 500 was poised for a small gain when trading begins, after reaching a record on Thursday. The Stoxx Europe 600 was 0.6 percent higher, and the FTSE 100 in Britain dipped slightly. In Asia, the Nikkei 225 in Japan closed with a gain of 2.4 percent, climbing to a level it last hit in 1990.

-

Though Washington continues to reverberate after a pro-Trump mob overran the Capitol building on Wednesday, the investing world is instead focused on the prospect for another round of federal stimulus spending to bolster the economy, as Democrats assume leadership of the White House and both houses of Congress.

-

“Now you have the potential for more stimulus, even possibly an infrastructure spend,” said Kristina Hooper, chief global market strategist at the investment management firm Invesco on Thursday. “So, I think the stock market is enthused right now. And that enthusiasm is pretty strong.”

-

Investors also seemed to look past the Labor Department’s report on December payrolls, which showed U.S. employers cut 140,000 jobs last month, the first drop since last spring. The weak report bolsters the argument that more economic stimulus is needed.

-

Gains continued in other financial markets too. Oil prices continued their rally, with Brent crude climbing 1.6 percent, to $55.25 a barrel, and West Texas Intermediate rallying to above $51 a barrel.

The federal government released updated rules for lenders just before midnight on Wednesday for the next round of Paycheck Protection Program lending, but it did not set a date for when it expects to begin taking applications.

Lenders anticipate the program could restart as soon as next week. Last month’s stimulus package included $284 billion for new loans through the small-business relief program, which ended in August after distributing $523 billion to more than five million businesses. In this next round, the hardest-hit business — those whose sales have dropped at least 25 percent from before the pandemic — can qualify for a second loan. First-time borrowers will also be eligible for loans.

The Small Business Administration, which runs the program, plans to give small lenders a head start. In its first two days, the program will accept loan applications only from community lenders like Community Development Financial Institutions, which specialize in working with low-income borrowers and in areas underserved by larger lenders.

For second loans of more than $150,000, applicants will need to provide their lender with records proving their sales have declined. Lenders will need to do a “good faith review” of those documents, but will be allowed to rely on borrowers’ certifications that their claims are accurate — a win for lenders, which are concerned about being held liable for fraudulent claims.

For smaller loans, borrowers will not need to provide their sales records as part of their application, but the S.B.A. can request them later.

The S.B.A. is scrambling to release a variety of relief measures included in last month’s stimulus bill, including a $15 billion grant program for music clubs, theaters and other live-events venues. The agency has not yet released any details on that program, and it will not start until after President-elect Joseph R. Biden Jr. takes office.

Several states say they are moving quickly to restore federal unemployment benefits that lapsed last month when President Trump delayed signing a second round of federal pandemic relief.

A handful, including New York, Texas, Maryland and California, say they have started sending out the weekly $300 supplement that was part of the legislation, while others like Ohio say they are awaiting more guidance from the U.S. Labor Department.

Michele Evermore, a senior policy analyst at the National Employment Law Project, said that “at least half of the states should have something up by next week.”

Congress approved 11 weeks of additional benefits, and the entire amount will ultimately be delivered to eligible workers even if payments are initially delayed.

“Any claims for the first week will be backdated,” said James Bernsen, deputy director of communications at the Texas Workforce Commission.

In addition to a $300-a-week supplement for those receiving unemployment benefits, the $900 billion emergency relief package renews two other jobless programs created last March as part of the CARES Act.

One, Pandemic Unemployment Assistance, covers freelancers, part-time hires, seasonal workers and others who do not normally qualify for state unemployment benefits. A second, Pandemic Emergency Unemployment Compensation, extends benefits for workers who have exhausted their state allotment.

This latest round also offers additional assistance for people who cobble together their income by combining a salaried job with freelance gigs. The new program, called Mixed Earner Unemployment Compensation, provides a $100 weekly payment to such workers in addition to their Pandemic Unemployment Assistance benefits.

-

Boeing agreed to pay more than $2.5 billion in a legal settlement with the Justice Department stemming from the 737 Max debacle, the government said on Thursday. The agreement resolves a criminal charge that Boeing conspired to defraud the Federal Aviation Administration, which regulates the company and evaluates its planes. With less than two weeks left in the Trump administration, the agreement takes the question of how a Biden Justice Department would view a settlement off the table. President Trump had repeatedly discussed the importance of Boeing to the economy, even going so far last year to say he favored a bailout for the company.

-

Elon Musk, the chief executive of Tesla and SpaceX, is now the richest person in the world. An increase in Tesla’s share price on Thursday pushed Mr. Musk past Jeff Bezos, the founder of Amazon, on the Bloomberg Billionaires Index, a ranking of the world’s 500 wealthiest people. Mr. Musk’s net worth was $195 billion by the end of trading on Thursday, $10 billion more than that of Mr. Bezos’s. Mr. Musk’s wealth has increased by more than $150 billion over the past 12 months, thanks to a rally in Tesla’s share price, which surged 743 percent in 2020. The carmaker’s shares rose nearly 8 percent on Thursday.

-

Wayfair, the furniture and home goods e-commerce business, said on Thursday that all of its U.S. employees would be paid at least $15 an hour. The increase, which took effect on Sunday, applies to full-time, part-time and seasonal employees. More than 40 percent of Wayfair’s hourly workers across its U.S. supply chain and customer service operations received a pay bump.

-

The Tiffany-LVMH saga has finally come to a well-polished, multifaceted end. LVMH, the French conglomerate, completed its acquisition of the American jewelry brand on Thursday, and it was out with the old and in with the new — executives, anyway. After a brief transition period, gone will be Reed Krakoff, Tiffany’s chief artistic officer. Also leaving will be Daniella Vitale, the chief brand officer. In their place comes Alexandre Arnault, who will become executive vice president, product and communications.

{kind=link}